Yes, you can lease a used car, often called a certified pre-owned lease.

If you have wondered can you lease a used car, you are not alone. I have helped many drivers compare used leases with buying and new leases. In this guide, I break down how it works, the costs, and the traps to avoid. By the end, you will know when a used lease fits your budget and lifestyle, and when it does not.

How Used Car Leasing Works

Can you lease a used car through a dealer or a bank program? Yes. Most used leases come from certified pre-owned vehicles that just came off lease. They have low miles, a clean history, and are reconditioned. Some banks also lease non-certified used cars, but rules are stricter.

Here is the basic flow:

- The lender sets a residual value. This is what the car should be worth at lease end.

- You pay for the car’s expected drop in value during your term. That is the depreciation part.

- Add rent charges. This is like interest.

- You choose miles per year. Common choices are 10,000 to 15,000.

- At the end, return the car or buy it at the set price.

Used leases tend to be shorter. Many are 24 to 36 months. The warranty may cover much of your term, which helps with surprise repair costs.

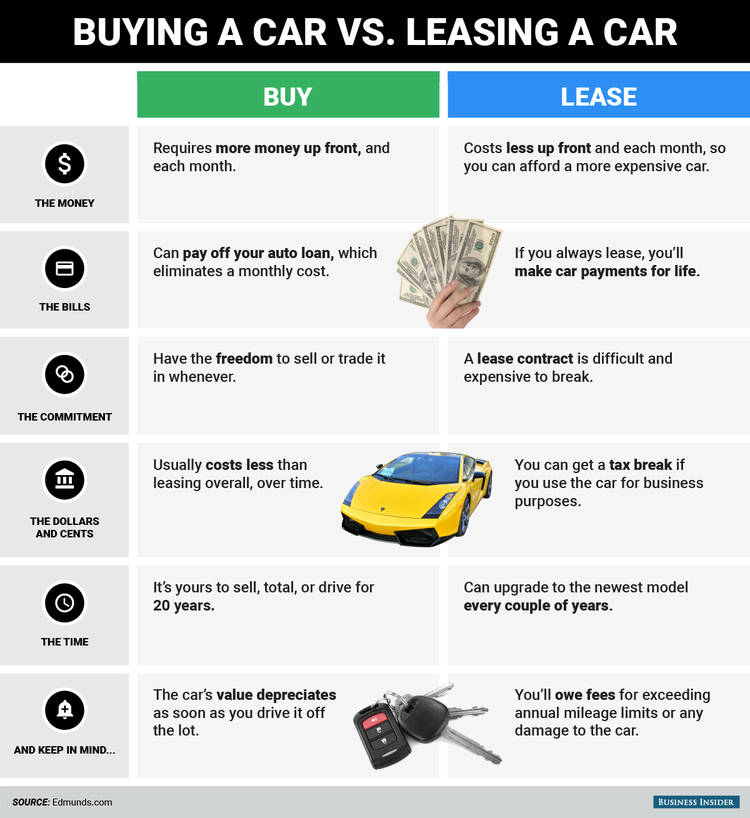

Pros and Cons of Leasing a Used Car

People ask, can you lease a used car to save money right away? Often, yes. But it depends on the model, miles, and terms.

Pros

- Lower monthly payment. The car already took its biggest hit in value.

- Lower sales tax in many states. You pay tax on the monthly payment, not the full car price.

- Shorter terms. You can upgrade sooner.

- Certified warranty coverage. Many CPO cars carry strong protection.

Cons

- Higher maintenance risk if the car is out of warranty.

- Limited selection. Not many lenders offer used leases on every brand.

- Stricter inspection standards. Wear and tear fees can add up at turn-in.

- Money factor may be higher than new leases.

In my work, the best used leases were on popular models with stable values. Think small SUVs and reliable sedans.

Costs and Math: Payments, Residuals, and APR

A common question is, can you lease a used car and still get a great rate? You can, but used rates are often a bit higher than new.

Key cost parts:

- Capitalized cost. This is the sale price you negotiate.

- Residual value. The set buyout at the end of the term.

- Money factor. The lease’s interest rate, shown in a different format.

- Fees. Bank fee, doc fee, registration, and sometimes disposition.

Simple way to view the math:

- Depreciation portion. Sale price minus residual, divided by months.

- Finance portion. Money factor times the sum of price and residual.

Example

- Sale price 24,000. Residual 16,000 after 36 months.

- Depreciation is 8,000 over 36 months, or about 222 per month before fees and finance.

- Add finance and fees to get the full payment.

Tip from the desk: focus on the sale price first. Then confirm the residual and money factor in writing. Ask for the base rate without markups.

Where to Find Used Car Leases

Can you lease a used car from any dealer? Not always. Target the right places.

Best sources

- Franchised dealers. Ask for certified pre-owned lease programs.

- Lender partners. Some banks and credit unions offer used lease options.

- Lease assumption platforms. Take over a lease with months left and a set payment.

- Brokers. They can shop lenders and find niche programs.

Call ahead and ask, do you offer used car leases on the brand I want? Inventory moves fast, so be ready to act when you find a match.

Eligibility, Credit, and Requirements

Can you lease a used car with fair credit? Sometimes yes. Lenders still check credit, income, and debt levels. Strong credit helps you get the base money factor and lower fees.

Typical requirements

- Proof of income and residence.

- Insurance that meets the lender’s limits.

- A down payment is not required, but drive-off fees are. You can roll many fees into the payment.

If your credit is thin, bring more proof. Pay stubs, bank statements, or a co-signer can help. Also, choose a model with solid resale. It can improve approval odds.

:max_bytes(150000):strip_icc()/personal-finance012915car-leases-should-you-take-purchase-option.aspfinal-20bb2476f7694316bf97e1af57037975.jpg)

How to Compare a Used Lease vs Buying Used

Many shoppers ask, can you lease a used car instead of buying to lower risk? It can lower risk if the car is under warranty and you plan to keep it short term.

Compare on these points

- Total cost over the same time. Add payments, tax, fees, and expected repairs.

- Warranty coverage. See if the lease term lines up with the CPO warranty.

- Flexibility. A lease locks miles and conditions. Buying gives more freedom.

- Buyout value. If you love the car, can you buy it for a fair price at the end?

If you drive many miles, buying often wins. If you want a lower payment and newer tech every few years, a used lease can fit.

Step-by-Step Checklist to Secure a Good Used Lease

Can you lease a used car and avoid costly mistakes? Yes, if you follow a clear process.

- Set your budget. Include payment, insurance, and fuel.

- Pick three models. Research reliability, resale value, and CPO coverage.

- Get pre-approval. Check rates from a bank or credit union.

- Ask dealers for a full lease worksheet. Compare sale price, residual, money factor, and fees.

- Inspect the car. Review the service history and get a pre-purchase inspection if possible.

- Match miles to your life. Do not understate miles to chase a lower payment.

- Negotiate the sale price like a cash deal. Then confirm the money factor and fees.

- Review the buyout value and fees at the end. Make sure it is in the contract.

- Sign only when numbers match the agreed worksheet.

This simple path saves time and stress. It also helps you compare offers apples to apples.

Mistakes to Avoid and Insider Tips

People wonder, can you lease a used car without hidden costs? You can, if you know where the costs hide.

Mistakes to avoid

- Skipping the inspection. Small issues can become big turn-in fees.

- Choosing the wrong mileage plan. You pay more per mile at turn-in.

- Ignoring tires and brakes. Worn parts trigger fees.

- Letting money factor markups slide. Always ask for the base rate.

Insider tips

- Target late-model CPO units. They balance price, warranty, and selection.

- Watch for models with strong resale. Think reliable brands and trims with demand.

- Use lease assumptions for short terms. This can avoid upfront fees and lower risk.

- Ask for a wear-and-tear waiver. Some lenders include one. It can save you at turn-in.

These small moves can make or break the deal. I have seen buyers save thousands with them.

Real-World Examples and Scenarios

Clients often ask, can you lease a used car that still feels new? Yes, and these examples show how it can play out.

Scenario 1: Budget SUV for a growing family

- A two-year-old compact SUV with 24,000 miles.

- Certified warranty to 6 years or 100,000 miles, depending on brand.

- Payment 15 to 25 percent lower than a new lease on the same model.

Scenario 2: A short-term lease for a job assignment

- Lease assumption with 12 months left.

- Low upfront costs and a clear end date.

- Ideal when you need a car now but not for long.

Scenario 3: Value sedan with a focus on total cost

- Three-year-old sedan with strong resale.

- Lower payment than new, but plan for tires and brakes during the term.

- Buyout option lets you keep the car if you love it.

These cases show when used leasing shines. It suits people who want a lower payment and short commitment.

Frequently Asked Questions of can you lease a used car

Can you lease a used car with bad credit?

You might, but terms may not be ideal. A larger security deposit or a co-signer can help.

Where can you lease a used car?

Start with franchised dealers and ask about CPO leasing. Also check lease assumption sites for short terms.

Can you lease a used car if you drive a lot?

Heavy drivers often pay more in mileage fees. Consider a higher-mile plan or buy instead.

Is insurance higher on a used lease?

Insurance needs to meet lender limits. Rates depend on the car’s value, your history, and coverage.

Can you buy the car at the end of a used lease?

Yes, if your contract includes a buyout price. Compare that price to the car’s real market value.

Can you lease a used car without a down payment?

Many leases do not require a down payment. You still pay drive-off fees unless you roll them into the payment.

Conclusion

Leasing a used car can lower your payment, shorten your term, and keep you in a newer vehicle with solid coverage. It works best on models with strong resale and clean histories. The key is to confirm the price, the rate, the fees, and the buyout in writing, and to choose the right miles for your life.

If you are ready, gather two or three offers and compare them line by line. Use the checklist above, ask the dealer to share the full worksheet, and push for the base rate. Want more tips like this? Subscribe, share your questions, or tell me what you want me to break down next.

1 thought on “Can You Lease A Used Car: Costs, Pros & Cons For 2026”